02 9683 5999

02 9683 5999

In this update we review the June quarter, review the inflation and interest rate outlook both in Australia and globally and look at the next Capex supercycle.

June Quarter

Equity markets in Australia consolidated after two strong previous quarters. US technology companies continued to perform strongly.

The best performing sectors for the quarter were Utilities (+12.1%), Information Technology (+2.8%), and Financials ex property (+2.7%). The worst performers were Energy (-6.9%), Property (-6.8%), and Materials (-5.9%). The top contributors to the ASX 200 were Commonwealth Bank of Australia (+39.5), National Australia Bank (+16.6), Westpac Banking Corporation (+15.0), Aristocrat Leisure (+14.5) and CSL (+11.8). The bottom five contributors were BHP Group (-27.0), Fortescue Ltd (-24.4), James Hardie Industries PLC (-21.0), Woodside Energy Group Ltd (-14.6) and Wesfarmers (-12.3).

During the quarter Macquarie Group hosted a conference where 114 companies presented over 3 days. Commonly referred to as ‘Confession Season’, companies take this opportunity to inform the market on any updates to operations as we near the end of FY24. On this occasion changes to guidance were rare.

Key highlights from the Macquarie conference.

- Artificial Intelligence was mentioned in virtually all presentations and seems destined to become a key differentiator in company performance in future years.

- Most presenters remain positive on Australia’s longer-term prospects (population growth, abundant commodities, healthcare system, education, strong employment). However, many referred to shorter-term headwinds – specifically a lack of skilled workers in certain areas, high wage costs, housing shortage, and the impact of high interest rates on a portion of consumers.

- Blackstone noted that they are not overly concerned with the outcome of the U.S. presidential election or the stability of the political system. Their greatest concern is the impact of ever-increasing budget deficits in key developed economies and the impact they will have on the stability of financial markets.

- The Australian banking system is in very good shape, but currently lacking growth prospects. Potentially AI can make a difference from a productivity perspective.

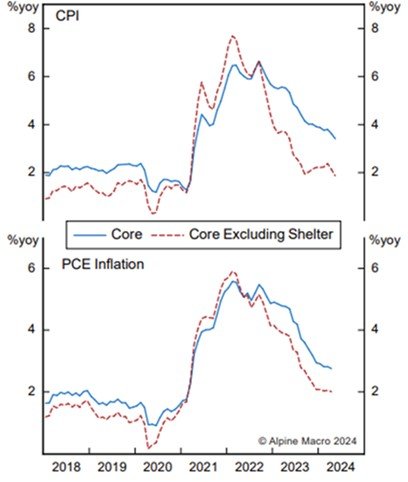

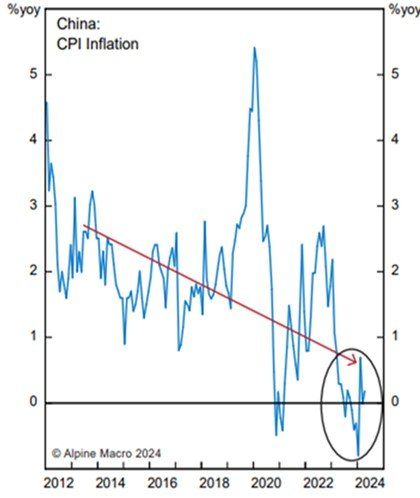

Global Inflation is past the peak

Global inflation is past the peak, in part courtesy of goods price deflation from China. In China the combination of rising productivity growth and a lack of domestic demand means price declines on many Chinese manufactured products. China’s rapid pace of automation sees it now rival Japan in relation to use of robotics per 100 workers. This has resulted in productivity growth for the Chinese economy of nearly 6% per annum since 2015. The impact of China’s continued, large productivity advances will be enormous for the rest of the world. Chart 2 shows that China may stay in a deflationary environment for longer, and this will likely sustain global goods deflation.

Chart 1 – US Underlying Inflation Downtrend

Chart 2 – China Inflation Downtrend

Source – Alpine Macro

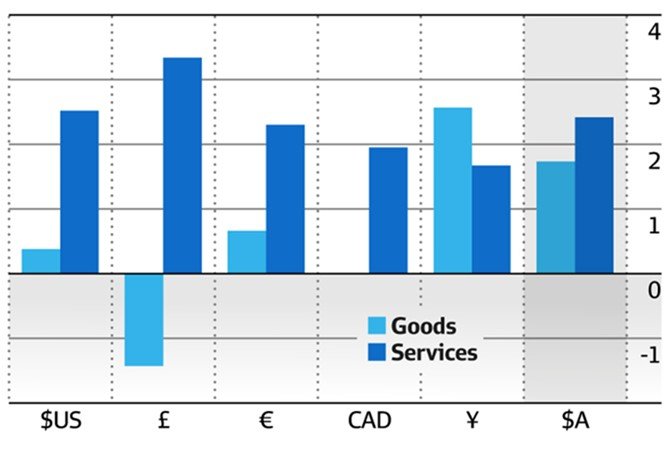

Australia’s inflation remains elevated

In Australia inflation remains elevated. As chart 3 shows both goods and services inflation remain high.

Chart 3 – Goods and Services Inflation (%)

Source – PriceStats

Service inflation is tied to wages and labour markets. Australia’s unemployment rate is currently 4%, which remains below the RBA’s natural rate of unemployment of 4.25%. This means a tight labour market, as demand is greater than supply. Australian job vacancies fell 2.7% quarter on quarter in the three months to May. The outcome marked the 8th consecutive quarterly decline, with vacancies now 24.0% below their peak in 2022. In June, Australia’s Fair Work Commission (FWC) announced that Award and Minimum wages will increase +3.75% on 1 July 2024. The decision will impact ~25% of employees and ~11% of the total wages bill in Australia. The outcome was well below last year’s increase of +5.8% and supports the view that wage-sensitive services inflation should ease over 2H2024, particularly across the hospitality sector.

In relation to goods inflation a stronger Australian dollar would help stamp it out. To get it, the RBA could either raise rates or sit tight while others (most importantly the US Federal Reserve) cut first.

Central Banks Dual Mandate

The RBA recently noted that Australia has added 2.7 million people to the workforce over the past decade. Easing in labour demand is expected to push Australia’s unemployment rate up to 4.6% by end 2024. Both the RBA and the US Fed continually refer to their dual mandate, of wanting to get inflation down while maintaining employment growth.

Canada and several European economies have begun cutting interest rates. At the time of writing the probability of a US rate cut in September, is between 60 per cent and 70 per cent, according to CME futures. It’s at 77 per cent for November and 94 per cent for December. Core PCE is now averaging below the US Fed’s latest projections, which are two-to-three cuts in the next year. The Fed has the green light to cut.

In Australia the major banks are split on their projections, with Commonwealth Bank and Westpac forecasting the RBA to slash the cash rate in November this year. National Australia Bank expects easing in May 2025 and ANZ in February next year. RBC Capital Markets chief economist Su-Lin Ong described the RBA as a “reluctant hiker” that was keen to protect the labour market as much as possible.

Needless to say, equities will move higher if inflation declines, the economy avoids recession, and the US Fed steadily cuts interest rates.

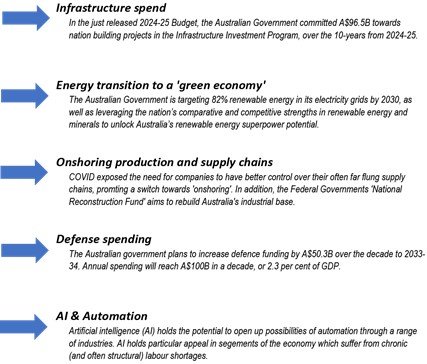

New Capex Supercycle.

In Australia twin peaks of population growth and baby boomer spending have insulated the economy and investors against rate hikes. Now a new tailwind is emerging. Australian business investment rose to a near nine-year high in the March quarter as telecoms companies ramped up spending on data centres, while plans for future investment were also upgraded in a boost for the longer-term economic outlook.

The new capex supercycle is being driven by five factors: $96.5 billion worth of federal government infrastructure spending over the next decade; the complex and expensive energy transition; onshoring of supply chains, supported locally by the government’s National Reconstruction Fund; massive defence spending; and the artificial intelligence and automation boom.

Chart 4 – Drivers of the next capex ‘supercycle’

Source – Goldman Sachs

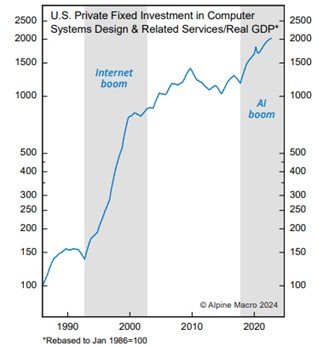

In the US, Chart 5 shows that the strong upswing in private capital investment in technology related hardware and software is mimicking what happened in the 1990s. The internet lifted U.S. labor productivity by about 1-1.3% per year from the second half of the 1990s to the first half of the 2000s, creating a sustained disinflationary boom. It appears that AI could do a similar trick for the U.S. economy. U.S. non-financial sector productivity is rising at a 3.5% annual rate, a very high level for a well-developed economy.

Chart 5 – AI driven CAPEX Boom in US Private Fixed Investment in Computer Systems

Source – Alpine Macro

Investment Strategy – There are always opportunities in Stock/Sector Selection

Considering the market’s robust start to 2024 and the concentrated strength in specific stocks and sectors, attention is now drawn to areas that have been relatively overlooked. Healthcare, which has recently underperformed, presents a low-risk entry point for new capital. Defensive sectors, including Consumer Staples, and Resources, have lagged offering potential opportunities.

We continue to hold a balanced portfolio structure across Growth (Information Technology, Logistics, Healthcare, International), Defensives (Consumer Staples, Infrastructure, Gold) and Cyclicals (Resources, select Financials).

For assistance or guidance managing your investment portfolio, contact CIB Private Wealth Director Paul Israel on 02 8274 5807.